- Call for Consultation: 212-843-4059 Tap Here to Call Us

Buy Sell Agreements (Cross Purchase and Stock Redemption)

The insured buy-sell agreement is a good solution to the problem of close corporation management continuity. No other plan carries with it the same degree of assurance that the purposes of the plan will be achieved.

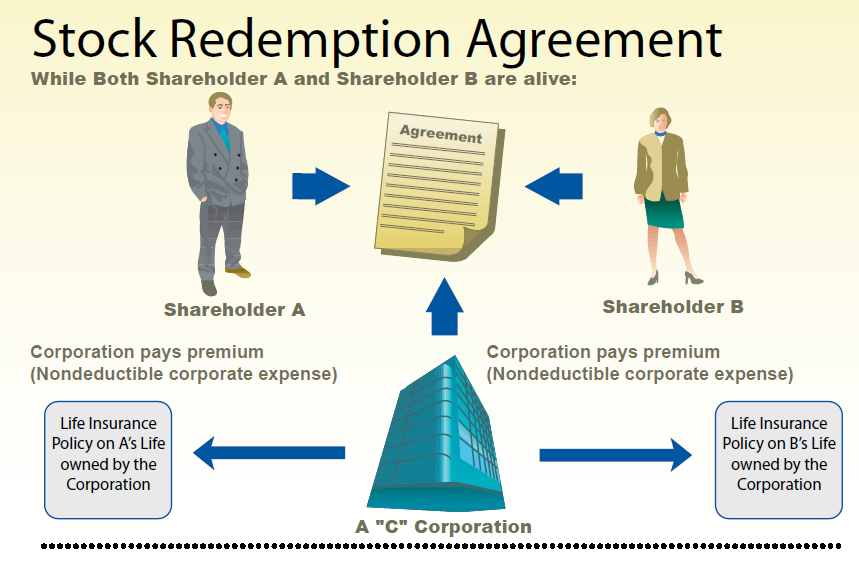

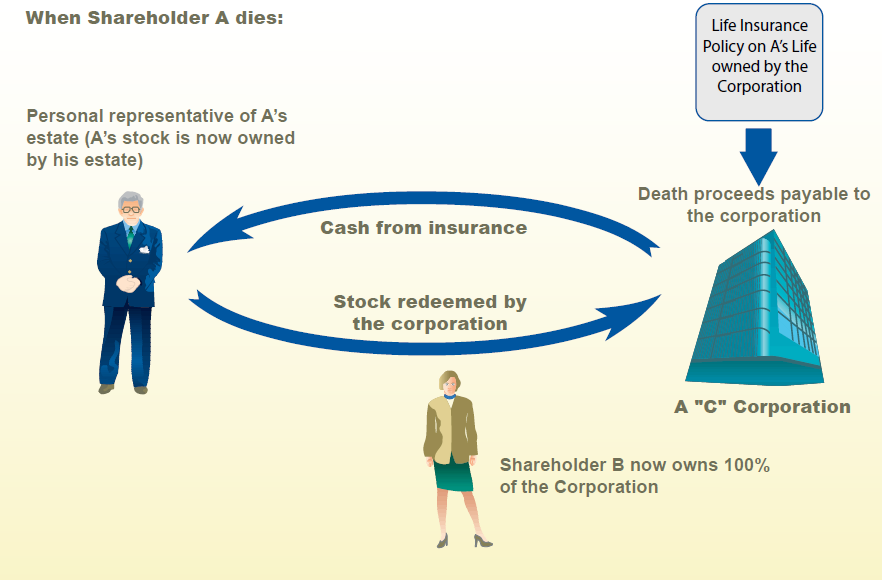

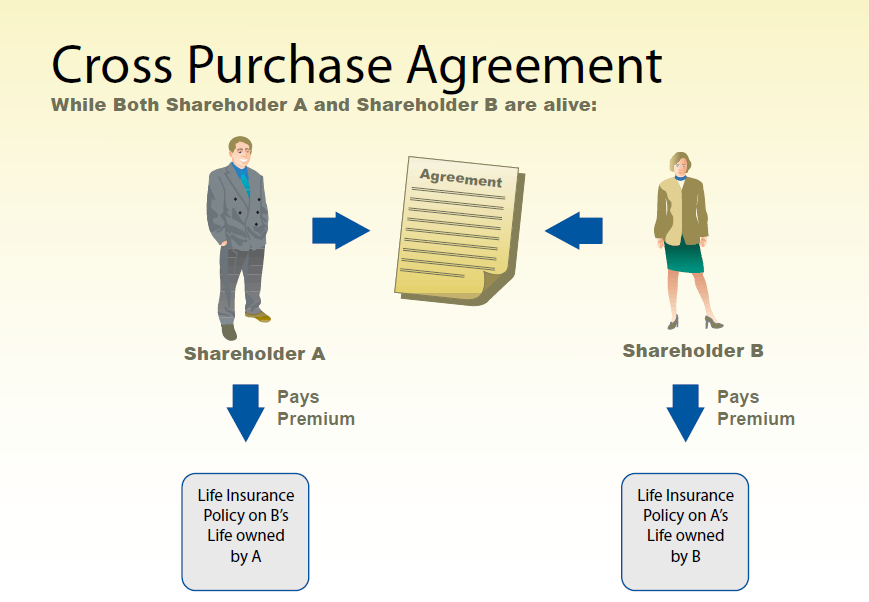

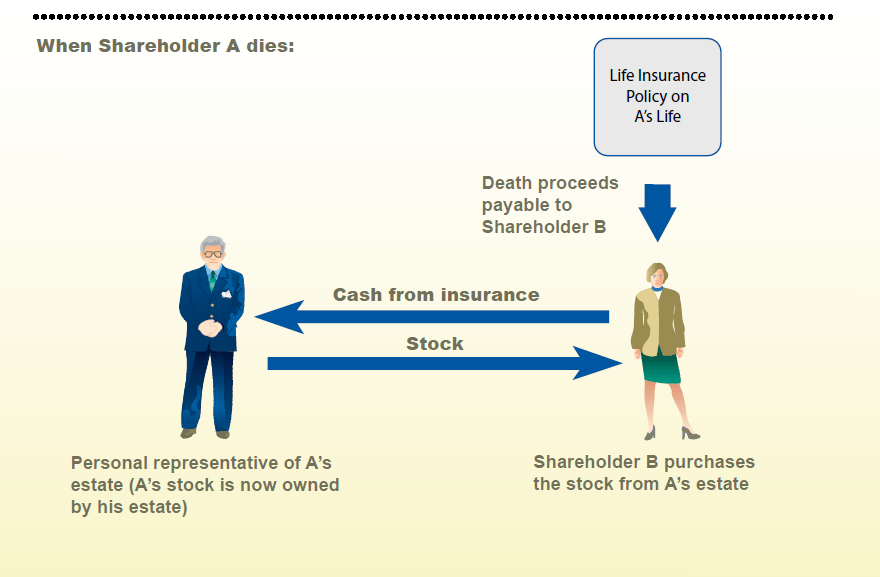

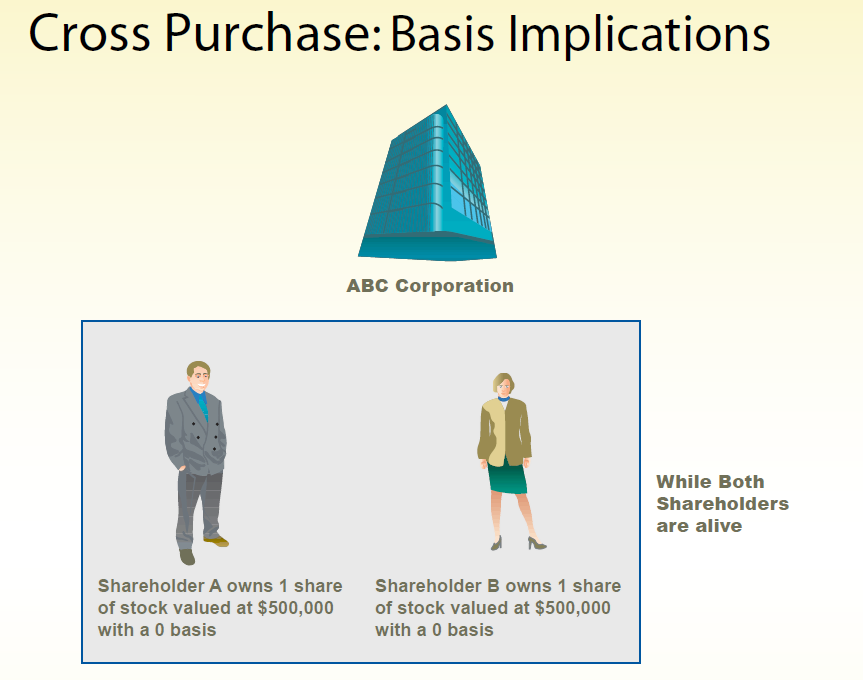

The plan is simplicity itself. Under it, the stockholders enter into a binding buy-sell agreement among themselves. They contract to purchase the interest of any stockholder who dies; each stockholder agrees and contracts for the sale of his or her interest at death (a so-called Cross Purchase Agreement — see graphic above). Alternatively, the agreement may be between the stockholders and the corporation, obligating the corporation to purchase the shares of a deceased stockholder and either hold the shares as treasury stock or retire them (a so-called Stock Redemption Agreement — see graphic below). The factors to be considered in choosing between these two types of agreements must be carefully considered.

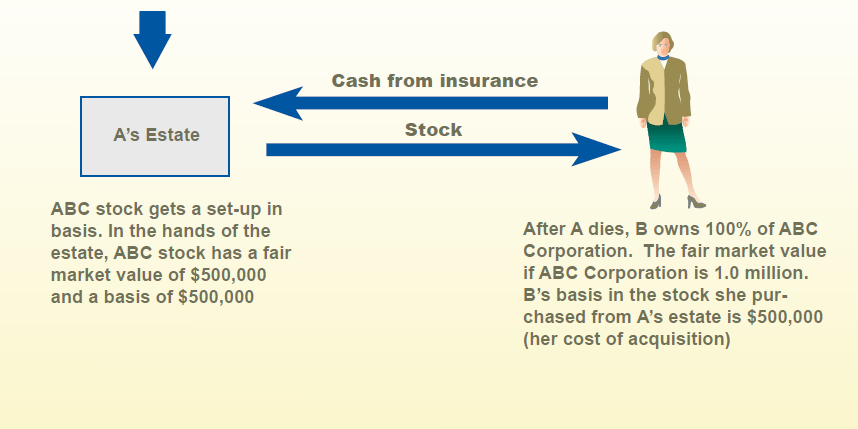

The agreement is automatically effective at death. The surviving stockholders, in a Cross Purchase Agreement (or the corporation in a Stock Redemption Agreement) are assured the right to buy the stock and thus keep management control in the survivors. The estate and the heirs do not enter the business, either as active or inactive stockholders. They are bought out automatically under the agreement.

A price, or method of establishing the price, is set out in the agreement. There is no post-death haggling over price or terms. The amount to be paid for the deceased’s stock is set out in the contract, and the terms of payment are agreed upon in advance.

The plan involves a definite agreement for the surviving stockholders (or corporation) to buy and for the estate to sell. The obligations are binding on both sides, therefore neither side can take advantage of the other.